Raumbeispiel

344

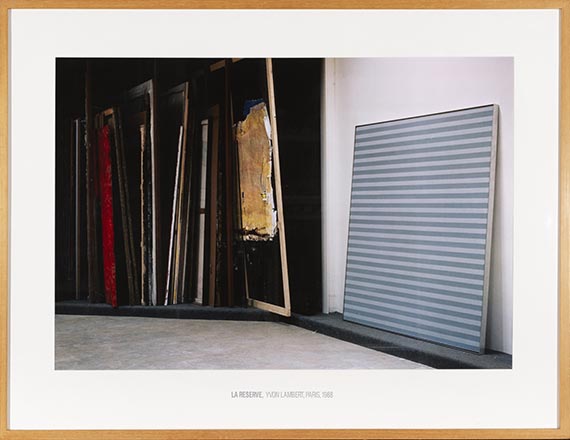

Louise Lawler

La Reserve, 1988.

Cibachrome print

Estimate:

€ 18,000 / $ 20,700 Sold:

€ 30,480 / $ 35,052 (incl. surcharge)

344

Louise Lawler

La Reserve, 1988.

Cibachrome print

Estimate:

€ 18,000 / $ 20,700 Sold:

€ 30,480 / $ 35,052 (incl. surcharge)

La Reserve. 1988.

Cibachrome print.

Signed, dated, numbered and with the artist's address stamp on the reverse. From an edition of 5 copies. Visible area: 68.6 x 100 cm (27 x 39.3 in).

Not unframed for cataloging. [EH].

• Louise Lawler keenly observes the paths that artworks follow after their creation.

• Like Cindy Sherman, she adopts a postmodern conceptual approach in her work – as a voyeur in the art world.

• The artist's works are represented in the collections of Tate Modern, London, Centre Pompidou, Paris, Los Angeles County Museum of Art, and Museum of Modern Art, New York, among others.

PROVENANCE: Metro Pictures Gallery, New York (with a typographically inscribed label on the reverse of the frame).

Private collection, Bavaria.

Cibachrome print.

Signed, dated, numbered and with the artist's address stamp on the reverse. From an edition of 5 copies. Visible area: 68.6 x 100 cm (27 x 39.3 in).

Not unframed for cataloging. [EH].

• Louise Lawler keenly observes the paths that artworks follow after their creation.

• Like Cindy Sherman, she adopts a postmodern conceptual approach in her work – as a voyeur in the art world.

• The artist's works are represented in the collections of Tate Modern, London, Centre Pompidou, Paris, Los Angeles County Museum of Art, and Museum of Modern Art, New York, among others.

PROVENANCE: Metro Pictures Gallery, New York (with a typographically inscribed label on the reverse of the frame).

Private collection, Bavaria.

Headquarters

Joseph-Wild-Str. 18

81829 Munich

Phone: +49 89 55 244-0

Fax: +49 89 55 244-177

info@kettererkunst.de

Louisa von Saucken / Undine Schleifer

Holstenwall 5

20355 Hamburg

Phone: +49 40 37 49 61-0

Fax: +49 40 37 49 61-66

infohamburg@kettererkunst.de

Dr. Simone Wiechers / Nane Schlage

Fasanenstr. 70

10719 Berlin

Phone: +49 30 88 67 53-63

Fax: +49 30 88 67 56-43

infoberlin@kettererkunst.de

Cordula Lichtenberg

Gertrudenstraße 24-28

50667 Cologne

Phone: +49 221 510 908-15

infokoeln@kettererkunst.de

Hessen

Rhineland-Palatinate

Miriam Heß

Phone: +49 62 21 58 80-038

Fax: +49 62 21 58 80-595

infoheidelberg@kettererkunst.de

We will inform you in time.