Frame image

Raumbeispiel

149

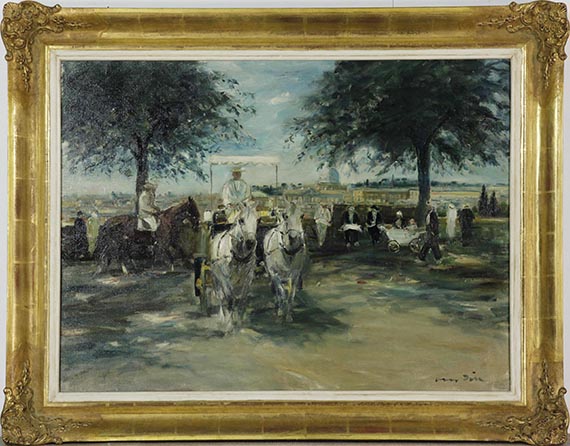

Otto Dill

Aus Rom, Um 1940.

Oil on canvas

Estimate:

€ 6,000 - 8,000

$ 6,600 - 8,800

Aus Rom. Um 1940.

Oil on canvas.

Signed lower right. Verso with the artist's address stamp and a titled label. 60.5 x 80.5 cm (23.8 x 31.6 in).

• A mise-en-scène of upper-class leisure activities, representing the city strolls of the 'flaneur' as an integral part of modern urban life.

Dill shows his virtuosity in depicting fleeting movement and the interplay of light and shadow in an elegant impasto style.

• Dill is considered one of the most important German late impressionists.

PROVENANCE: Private collection, Germany.

Called up: December 7, 2024 - ca. 14.04 h +/- 20 min.

Oil on canvas.

Signed lower right. Verso with the artist's address stamp and a titled label. 60.5 x 80.5 cm (23.8 x 31.6 in).

• A mise-en-scène of upper-class leisure activities, representing the city strolls of the 'flaneur' as an integral part of modern urban life.

Dill shows his virtuosity in depicting fleeting movement and the interplay of light and shadow in an elegant impasto style.

• Dill is considered one of the most important German late impressionists.

PROVENANCE: Private collection, Germany.

Called up: December 7, 2024 - ca. 14.04 h +/- 20 min.

149

Otto Dill

Aus Rom, Um 1940.

Oil on canvas

Estimate:

€ 6,000 - 8,000

$ 6,600 - 8,800

Buyer's premium, taxation and resale right compensation for Otto Dill "Aus Rom"

This lot can be purchased subject to differential or regular taxation, artist‘s resale right compensation is due.

Differential taxation:

Hammer price up to 800,000 €: herefrom 32 % premium.

The share of the hammer price exceeding 800,000 € is subject to a premium of 27 % and is added to the premium of the share of the hammer price up to 800,000 €.

The share of the hammer price exceeding 4,000,000 € is subject to a premium of 22 % and is added to the premium of the share of the hammer price up to 4,000,000 €.

The buyer's premium contains VAT, however, it is not shown.

Regular taxation:

Hammer price up to 800,000 €: herefrom 27 % premium.

The share of the hammer price exceeding 800,000 € is subject to a premium of 21% and is added to the premium of the share of the hammer price up to 800,000 €.

The share of the hammer price exceeding 4,000,000 € is subject to a premium of 15% and is added to the premium of the share of the hammer price up to 4,000,000 €.

The statutory VAT of currently 19 % is levied to the sum of hammer price and premium. As an exception, the reduced VAT of 7 % is added for printed books.

We kindly ask you to notify us before invoicing if you wish to be subject to regular taxation.

Calculation of artist‘s resale right compensation:

For works by living artists, or by artists who died less than 70 years ago, a artist‘s resale right compensation is levied in accordance with Section 26 UrhG:

4 % of hammer price from 400.00 euros up to 50,000 euros,

another 3 % of the hammer price from 50,000.01 to 200,000 euros,

another 1 % for the part of the sales proceeds from 200,000.01 to 350,000 euros,

another 0.5 % for the part of the sale proceeds from 350,000.01 to 500,000 euros and

another 0.25 % of the hammer price over 500,000 euros.

The maximum total of the resale right fee is EUR 12,500.

The artist‘s resale right compensation is VAT-exempt.

Differential taxation:

Hammer price up to 800,000 €: herefrom 32 % premium.

The share of the hammer price exceeding 800,000 € is subject to a premium of 27 % and is added to the premium of the share of the hammer price up to 800,000 €.

The share of the hammer price exceeding 4,000,000 € is subject to a premium of 22 % and is added to the premium of the share of the hammer price up to 4,000,000 €.

The buyer's premium contains VAT, however, it is not shown.

Regular taxation:

Hammer price up to 800,000 €: herefrom 27 % premium.

The share of the hammer price exceeding 800,000 € is subject to a premium of 21% and is added to the premium of the share of the hammer price up to 800,000 €.

The share of the hammer price exceeding 4,000,000 € is subject to a premium of 15% and is added to the premium of the share of the hammer price up to 4,000,000 €.

The statutory VAT of currently 19 % is levied to the sum of hammer price and premium. As an exception, the reduced VAT of 7 % is added for printed books.

We kindly ask you to notify us before invoicing if you wish to be subject to regular taxation.

Calculation of artist‘s resale right compensation:

For works by living artists, or by artists who died less than 70 years ago, a artist‘s resale right compensation is levied in accordance with Section 26 UrhG:

4 % of hammer price from 400.00 euros up to 50,000 euros,

another 3 % of the hammer price from 50,000.01 to 200,000 euros,

another 1 % for the part of the sales proceeds from 200,000.01 to 350,000 euros,

another 0.5 % for the part of the sale proceeds from 350,000.01 to 500,000 euros and

another 0.25 % of the hammer price over 500,000 euros.

The maximum total of the resale right fee is EUR 12,500.

The artist‘s resale right compensation is VAT-exempt.